I do know, you’re busy simply attempting to make a dwelling, paying that parking ticket, and coping with that consumer that’s having a meltdown. However let’s have a fast chat about tax charges. Not attractive, but it surely’s essential.

One of many greatest misunderstandings in private finance: Folks assume that when their revenue crosses into the next tax bracket, all of their revenue will get taxed at that larger charge.

Nope. Not the way it works.

This misunderstanding has value individuals actual cash — and worse, it’s scared them away from incomes extra.

The revenue tax system works like a layer cake. Every layer of revenue has its personal tax charge. As your revenue goes up, solely the {dollars} on that individual layer are taxed at that layer’s charge. The {dollars} you earned under it? They keep proper the place they’re, on the decrease charges. No person strikes.

Uncle Sam Provides Us the Backside Layer Tax-Free

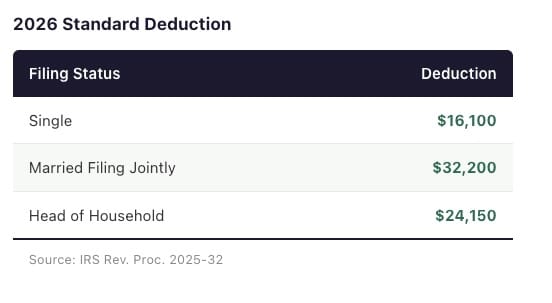

Earlier than the revenue tax charges take impact, we get to use the Normal Deduction or Itemized Deduction.

The Normal Deduction: No receipts. No spreadsheet. No tears. The primary portion of your revenue is diminished by a set quantity and never taxed in any respect.

The quantity will depend on your submitting standing. After the deduction, the tax charges within the desk above start to use.

Itemized Deduction: Should you assume itemizing will add as much as greater than the Normal Deduction, you itemize. This consists of gadgets akin to mortgage curiosity, property taxes, donations, medical bills (over a threshold quantity), and others. These are NOT enterprise bills; they’re calculated elsewhere. Stick with me.

The rule is straightforward: you decide whichever one is larger. If your itemized deductions add as much as greater than the usual deduction, you itemize. If not, you are taking the usual deduction and save your self the paperwork.

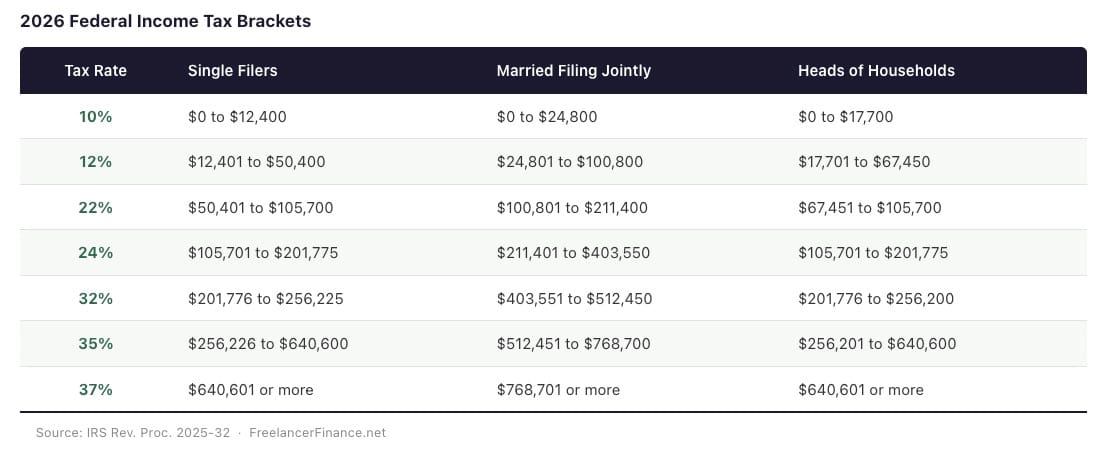

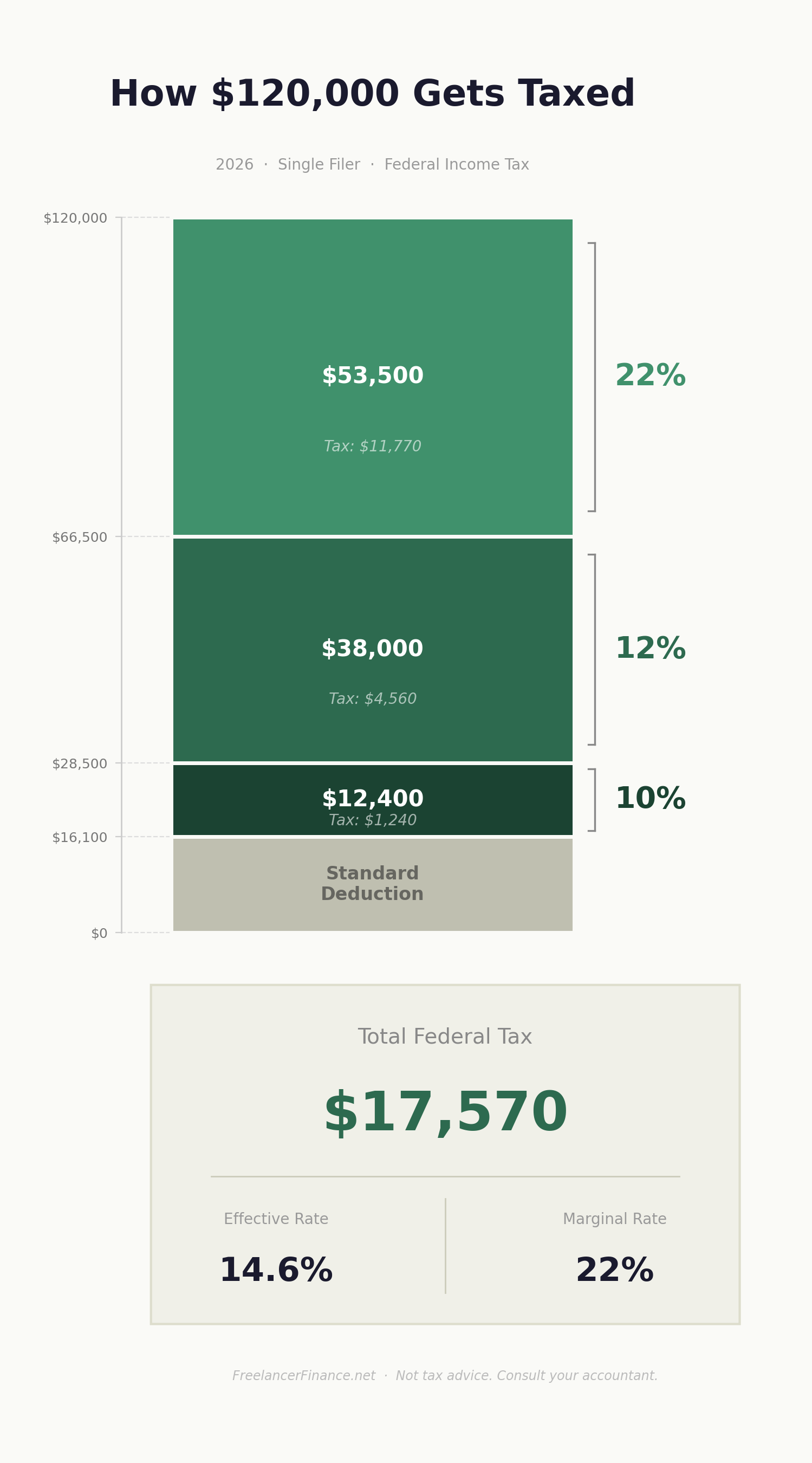

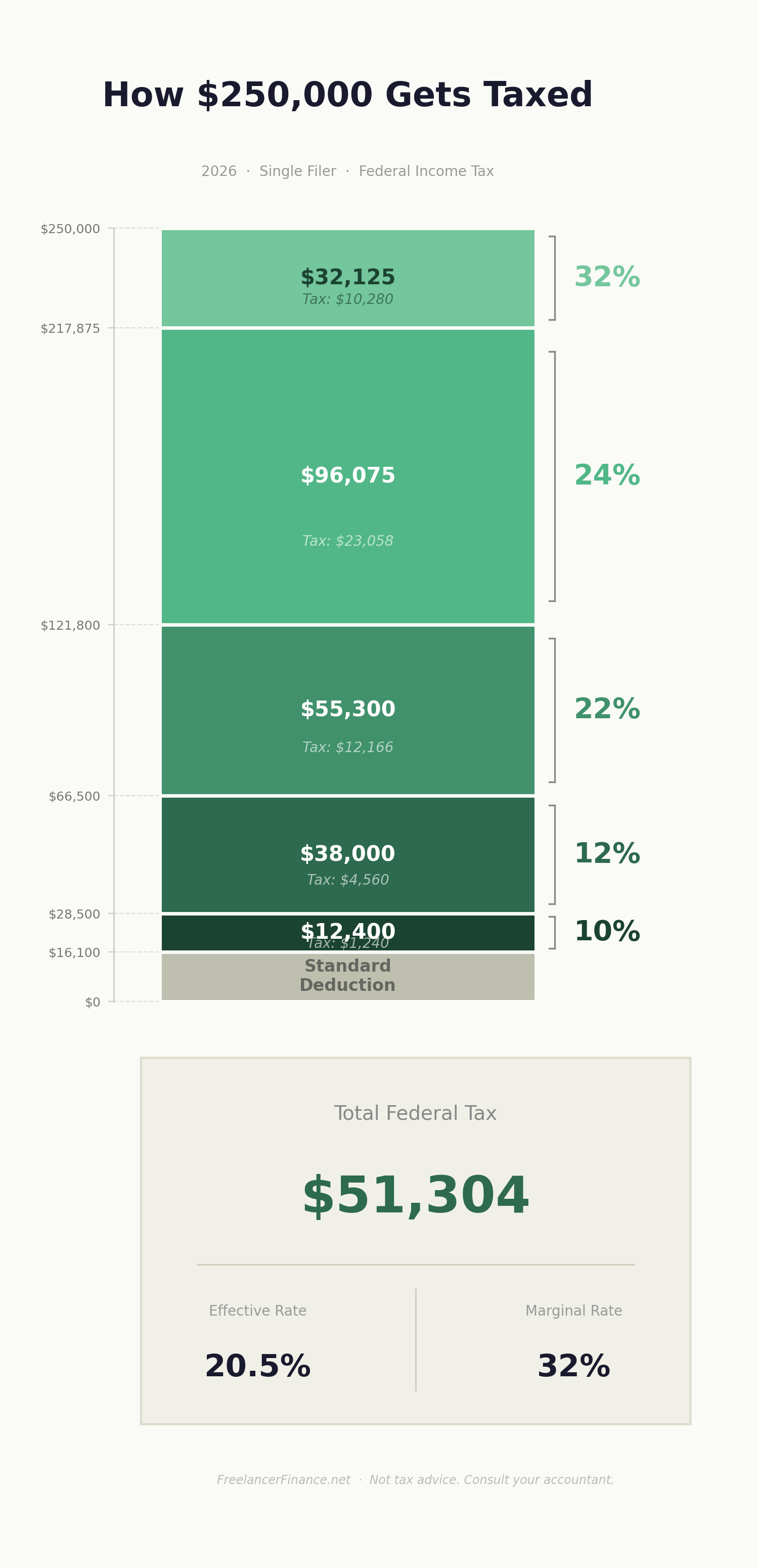

Single and Earned $120,000? Let’s Take a Look.

Right here is the ‘revenue cake’ and revenue tax charges on every layer if you’re submitting as single and earned $120k of Taxable Revenue.

Sure, this appears to be like totally different in comparison with the tax charges desk above, which begins at $0. That’s as a result of the IRS is referring to your taxable revenue, which begins AFTER the Normal or Itemized Deduction.

These are the layers:

- The primary $16,100 is free if you happen to’re taking the Normal Deduction, then:

- 10% tax on the primary $12,400 = $1,240

- 12% tax on the following $38,000 (from $12,401 to $50,400) = $4,560

- 22% tax on the remaining $53,500 (from $50,401 to $103,900) = $11,770

Complete federal revenue tax: $17,570

On $120,000 of gross revenue, you’re paying $17,570 in federal revenue tax.

Efficient Tax Price — the precise general proportion you paid — is 14.6%.

Marginal Tax Price — the highest tax charge you paid — is 22%. However that solely hits the final chunk.

This is the reason incomes more cash by no means ends in taking residence much less. You don’t pay extra tax in your whole revenue by incomes extra and shifting up into one other tax bracket. That fantasy must die. Making more cash, means making more cash!

You solely pay the upper charge on the {dollars} that cross into the following bracket.

Lower Off the High of the Cake — How Contributing to Your Pre-Tax Solo 401(ok) and HSA Lowers Your Taxes

That is the place it will get good. Whenever you contribute to a pre-tax Solo 401(ok) or a HSA, you’re slicing revenue straight off the highest of the cake, the best bracket. The costliest layer — gone, or not less than partially gone.

Utilizing our $120,000 instance: Let’s say you place $12,000 into your Solo 401(ok):

- You pulled $12,000 out of the 22% bracket ($12,000 × 22% = $2,640). That’s $2,640 of tax you pulled from the jaws of the IRS.

Higher but, that $12,000 you invested in your Solo 401(ok) (or IRA + HSA for a freelancer W-2 earner) will develop at a mean of round 7%. In 25 years, $12,000 rising at 7% turns into round $68,700. Do this yearly for 25 years and you find yourself with $1.04 million.

Yep. Isn’t compound curiosity a shocker?

What About State Tax?

In case your state has an revenue tax, it could be a flat tax like Illinois and Colorado. States akin to California, New York, and D.C. use the identical progressive, layered system because the federal authorities, however their tax charges and brackets differ by state.

In each circumstances, contributing to a Solo 401(ok) will decrease your state taxable revenue. PA and NJ have some bizarre guidelines re: retirement accounts, so be careful for them.

Don’t Neglect the HSA

The HSA additionally qualifies for a tax deduction and might additional cut back your taxable revenue. Use it for medical bills, or do what I do and use it as an funding account and let it develop. In 2026, you possibly can contribute:

- $4,400 for people

- $8,750 for a household

The cash stays yours. It’s not use-it-or-lose-it like an FSA. You could have a qualifying medical health insurance plan.

“I Will Simply Purchase Extra Tools for My Enterprise, So I Pay Much less Tax.” Perhaps Rethink That.

Should you actually NEED extra tools for your online business to make extra income, otherwise you’re bringing an tools buy ahead throughout a high-earning 12 months, then positive.

Your aim as a enterprise is straightforward: decrease bills, maximize revenue. Sure, you’ll pay tax on extra income, but it surely’s your cash to maintain. Spend slightly, make investments the remainder to create future wealth.

Your Solo 401(ok) — The Lengthy Sport

Right here’s the lengthy recreation:

By contributing to the Solo 401(ok) and HSA, you narrow the taxes you needed to pay, and your contributions develop untouched by the taxman for many years. You’ll ultimately pay revenue tax on withdrawals in retirement — however most individuals earn much less in retirement than throughout their peak incomes years. Which means your withdrawals will fall into decrease tax brackets, and also you’ll pay much less general.

The true energy? Tax-free, compound progress. Your full contribution grows 12 months after 12 months with out getting nibbled at by taxes alongside the way in which.

{kind=link}